Depreciation Expense in a Not for Profit Organization Should Be

For many who are first encountering the term it is a mysterious financial concept best considered only by CPAs. There are many methods of depreciation but there is little reason for a nonprofit to use any method other than the straight line method.

Depreciation Nonprofit Accounting Basics

The first answer is incorrect because SFAS No.

. This problem has been solved. Depreciation is seldom given the respect it deserves. Since depreciation is a tax-deductible non-cash expense you.

Depreciation expense is allocated to programs and therefore is a decrease in unrestricted net assets. Depreciate Your Way to a Healthier Nonprofit. Both incur expenses and some non-profits even have sales but the primary difference is taxation.

The straight line method works just like it sounds. Depreciation is expensed out each year as a non-cash expense on the statement of activities also known as the statement of operations. At Propel Nonprofits formerly Nonprofits Assistance Fund we hold depreciation among our favorite tools for building reserves and.

You can get away with Excel when you are first starting out and if your fixed asset list is small. The value of the fixed asset is depreciated evenly over the life of the asset. We review their content and use your feedback to keep the quality high.

Allocated to program but not support functions. Any purchases not meeting both of these criteria will be recorded as an expense. 93 requires depreciation of capital assets by not-for-profit organizations.

For example Fixed assets must cost 1000 or more and have a useful life of more than a year. Depreciation Expense In A Not For Profit Organization Should Be Points 5 Assigne assigned to or allocated to the functions to which it relatesreported under the management and general functiondisclosed in the notes to the financial statementsallocated to. Guidelines for keeping track of fixed assets over future years.

Non-profit organizations should record depreciation because it is a cost of doing business. Assigned to or allocated to the functions to which it relates. Calendar year entities December 31 2018.

Depreciation expense in a not-for-profit organization should be A. See the answer See the answer done loading. Year Four Record 200 to Depreciation Expense 200 to Accumulated Depreciation.

For example an organization purchases a computer for 99900 and. Criteria for recording fixed assets. Assigned to or allocated to the functions to which it relates.

Allocated to program but not support functions. Reported under the management and general caption. Experts are tested by Chegg as specialists in their subject area.

In not-for-profit organization depreciation is included in total expenses. The FASB states that depreciation expense in a not-for-profit organization should be. The term joint cost has a very particular meaning in the nonprofit world.

Reported under the management and general captionC. In practice many nonprofits use Excel to track depreciation. Disclosed in the notes to the financial statements.

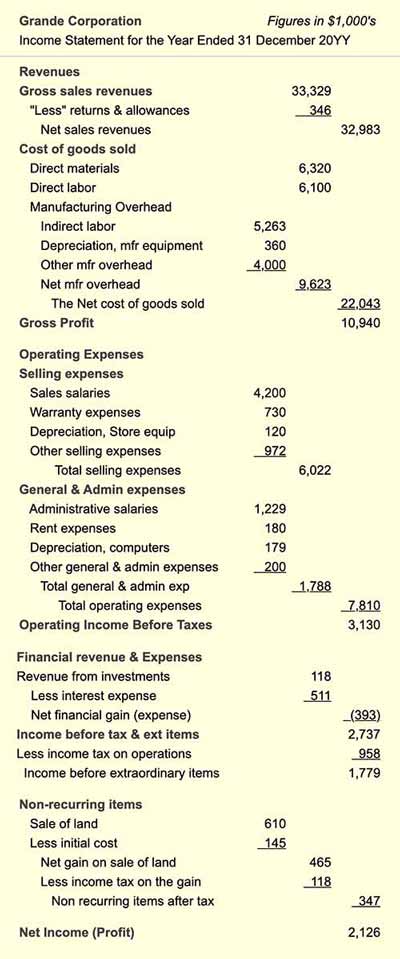

The first answer is incorrect because SFAS No. Total Expenses Before Depreciation 2375787 51795 3323316 507426 56754 3830742. Disclosed in the notes to the financial statementsD.

Disclosed in the notes to the financial statements. Disclosed in the notes to the financial statements. The FASB states that depreciation expense in a not-for-profit organization should be.

Assigned to or allocated to the functions to which it relates. A donor donated 10000 to nongovernmental non-for-profit organization and stipulated that this contribution should be. Depreciation expense in a not-for-profit organization should be A.

The FASB states that depreciation expense in a not-for-profit organization should be. Assigned to or allocated to the functions to which it relates. Statement of Position 98-2 Accounting for Costs of Activities of Not-for-Profit Organizations and State and Local Governmental Entities that Include Fund Raising.

The accumulated depreciation ie. On the contrary Grants to other organizations is not. The Financial Accounting Standards Board FASB requires nonprofit organizations to recognize the depreciation of property and assets in their financial statements.

Reported under the management and general function. Who are the experts. As a result churches that do not report depreciation will not be eligible for an unqualified opinion from a CPA at the.

Assigned to or allocated to the functions to which it relates. The FASB states that depreciation expense in a not-for-profit organization should be. Following is a deeper dive into not-for-profit functional expense reporting.

Regarding depreciation the argument was frequently made that profitability is not a goal of these organizations so that calculating and recording this expense was not needed. The sum of depreciation expense up to the reporting date is reported under the amount of the fixed asset on the statement of financial position of the non-profit organization. It refers to a cost that has components that include both program and fundraising.

A good capitalization policy should include at least two things. 93 requires depreciation of capital assets by not-for-profit organizations. Because there are no tax advantages to the non-profit many non-profits NPOs do not record depreciation.

Methods of Depreciation. Multiple Choice Reported under the management and general function. New required disclosures All organizations must report expenses by function and nature with a discussion of the.

It should be included as a decrease in unrestricted net assets. Depreciation Cost Salvage Value Useful Life of Assets Reporting Depreciation Expense Varies in NPOs. For most organizations this will not be an entirely new exercise as they have a statement or.

Allocated to program but not support functions. A not-for-profit NFP organization acting as a financial intermediary receives a contribution. Some college officials also contended that fund- raising campaigns rather than operations commonly financed new acquisitions so that ensuring the availability of adequate resources through the.

It should be included as a decrease in unrestricted net assets. Depreciation expense is allocated to programs and therefore is a decrease in unrestricted net assets. As many NFP organizations choose to present two years of financial statements now is the time to start thinking about how the new standard will impact your organization.

Effective date for all Not for Profit Organizations. Some organizations do not like writing off a non-cash expense and in some cases an organization can have a tight budget so they decide to change their policies and not account for depreciation as it decreases the overall revenue but they might have to reassess.

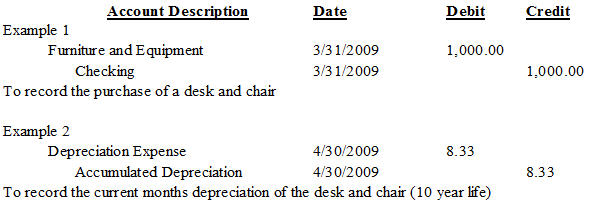

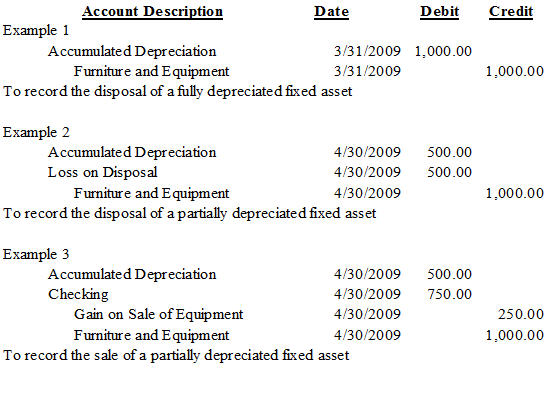

Depreciation Journal Entry Step By Step Examples Journal Entries Accounting Basics Accounting And Finance

Plus One Accountancy Notes Chapter 4 Bank Reconciliation Statement A Plus Topper Accounting Basics Accounting Notes Accounting Principles

Depreciation Nonprofit Accounting Basics

Depreciation Turns Capital Expenditures Into Expenses Over Time

Comments

Post a Comment